The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

Blind Spots: Pet Edition

In my 10+ years of coaching, though, I've realized that pets are one of the biggest financial blind spots for families.

I love dogs. I grew up with a dog and never pass up an opportunity to pet a random dog on the street. If the boys keep asking hard enough, we might actually get one for our household soon, too.

Buddy, my childhood friend, showing off part of his Michael Jordan jersey collection.

In my 10+ years of coaching, though, I've realized that pets are one of the biggest financial blind spots for families. It never fails. When I'm going through the initial budget with a new client, and we get to the pet category, the answer is always some form of, "Oh, we spend almost nothing on pets. Probably just a $50 bag of food every few months."

That's when my eyes get really, really big. Pet expenses are secretly crushing people's finances from right under their noses. Yeah, that bag of dog food might only cost $50, but all the other things we don't think about cost hundreds.....or thousands. And the vet expenses!!!! Here's what a typical vet expense monthly rhythm looks like: $0, $0, $0, $0, oh crap! That "oh crap!" moment is where the wheels fall off, and where the math works against us. Pets get sick. Pets get hurt. Pets make poor choices.

I didn't want this piece to be merely anecdotal, so I dug into my client files to find some real-world data. I looked up 8 active clients who have 2+ years of pet data. Here's what it looks like (in order of my research discovery):

$9,130 over 51 months = $179/month

$5,860 over 21 months = $279/month

$6,815 over 47 months = $145/month

$5,850 over 45 months = $130/month

$11,730 over 24 months = $489/month

$15,744 over 24 months = $656/month

$4,320 over 36 months = $120/month

$16,482 over 41 months = $402/month

In total, these eight randomized clients had an average monthly pet spend of just over $260/month. I don't know about you, but that's a tad bit different than a $50 bag of food every other month. These families range anywhere from $120/month to $656/month, with unexpected vet bills being the key driver of how high this category can get.

Pets are also one of the main culprits of credit card debt, as there's a deeply emotional component to this. When faced with a life-or-death decision regarding our beloved pets, it's hard to emotionally look ourselves in the mirror and put a rational price tag on our go/no-go decision. Thus, we simply act now and sort it out later. This is having some pretty harsh consequences for families.

Again, this isn't an indictment of pets or pet ownership. Rather, this is my encouragement to make decisions with our eyes wide open. It's totally okay to financially prioritize pets, but we ought to understand what we're really getting into from a financial perspective. The same goes for other categories, too! Eyes wide open is always the best approach. That way, our cute little pets (and all the other choices we make) can truly be blessings in our lives, and not pain points.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Two Families, Two Perspectives

I had a few interesting conversations last week that showcase an important concept. It's about two different families. Both families live in the same town. Both families have two kids under the age of 12.

I had a few interesting conversations last week that showcase an important concept. It's about two different families. Both families live in the same town. Both families have two kids under the age of 12.

Family 1:

The husband has a monthly take-home income of approximately $10,000.

The wife has a monthly take-home income of approximately $5,000

The total monthly take-home income is about $15,000

This family endures constant financial stress. There's rarely anything left over. The credit cards often come out to play. Most purchases are made with debt. There's very little savings, and giving seems like a pipe dream. Marital tensions are running high. Their overall sentiment is that if they just made a little more money, all of this financial stress would go away.

Family 2:

The husband has a monthly take-home income of approximately $5,000.

The wife stays at home with their two small children.

The total monthly take-home income is about $5,000.

This family's entire monthly income stream approximates the lower-income earner in Family 1. Their total take-home income is 1/3 of the other family's! Yet, they don't feel financial stress. No, there isn't a ton of extra each month, and they need to be diligent with the dollars they do have, but life is good! They consider themselves blessed, save for the future, and ensure giving is part of their monthly rhythm.

Would more money help? Yeah, it probably would. However, more isn't the answer. More isn't what defines our success. More isn't some magic pill that solves all of life's problems. This is a phenomenon I see over and over. Yes, more income can help, but 90% of our problems are the person staring back at us in the mirror, not the dollar amount on our paycheck. The sooner we realize this, the sooner we can take steps actually to improve our quality of life.

Final thought. Just imagine if we could do both. First, we get right with our relationship with money. We have a healthy mindset. We establish solid practices. We make the best use of every dollar we're blessed with.

Then, second, we find ways to increase our income along the way. We put in the work. We practice excellence. We pay our dues. We meet people's needs. We add value to the organization. When we do these things, additional income is a natural byproduct.

Combining these two ideas can literally revolutionize our lives. When we get right with money and put in the work, it's amazing what can happen!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Nothing Left Over

And just like every other time I have this chat, there's one part that stands out like a sore thumb: When I discuss the concept of having no income left over at the end of the month.

I had a wonderful chat with a young couple yesterday. They are an awesome young couple, but I'm biased. One of the spouses is a former youth group kid; I've known her since she was 15. Therefore, it's safe to say I'm tremendously honored to spend time with her now that she and her husband are living their full-on adult lives.

It was a similar conversation I've had with hundreds of couples. And just like every other time I have this chat, there's one part that stands out like a sore thumb: When I discuss the concept of having no income left over at the end of the month. If a couple starts the month with $4,000 of cash sitting in their checking account and has $7,000 of income coming in, they should end the month with $4,000 of cash sitting in their checking account. None of their income should be left over. All of it should be gone.

Here's why. We humans don't do well with "extra." Extra either gets squandered or hoarded, rarely an in-between. If there's extra, we'll impulsively spend it somewhere we didn't intend, or we'll squirrel it away for no specific purpose (which subconsciously incentivizes us to repeat and grow that behavior next time).

Here's how this could/should manifest itself in our monthly finances. Every dollar should have a home. We spend it, give it, or save it. If we get to the end of our budget and there's $500 left, we must go back up and find a place to spend it, give it, or save it. No dollar left behind!

I don't even care what people do with this extra money, so long as they are intentional about its destination. This one principle can revolutionize the way we perceive and handle money. Every bit of our income now has a purpose. Intentionality runs through our entire budget. The most important categories get love, not the most impulsive ones. This allows our personal values to shine through and become truly prioritized in our monthly finances. Things that should get funded actually get funded. Things that shouldn't, don't. It's simple. It's pure.

I started following this principle more than 20 years ago, and after teaching it to hundreds of families, I can positively testify that it's a real game-changer. Something to consider adding to your arsenal. Have an awesome day!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Reboot

Two of my clients completely fell out of their budgeting rhythm. Month after month after month of successful budget execution and tracking, followed by complete failure.

Two of my clients completely fell out of their budgeting rhythm. Month after month after month of successful budget execution and tracking, followed by complete failure. There are several reasons this can happen, but sometimes, life gets in the way, and the money stuff gets put on the back burner.

Here's what I recommend people NOT do: Try to catch up for the month(s) they missed. Trying to do so will most likely exacerbate the problem. Sometimes, people don't need a catch-up.....they need a reboot.

Here's what that looks like. Let the past be the past. Even if it means having blank months and unallocated transactions, just let it be. Don't try to rebuild last month, and don't even try to catch up on the current month, which is already halfway over. Instead, set your sights on the month to come. Recalibrate, negotiate what the future should look like, and get yourself ready for the new month. Then, once the first day of the next month strikes, execute well!

The idea of a reboot is so important. It requires us to give ourselves grace, forgive ourselves for the past, and focus 100% of our energy on the future. It's hard to drive forward when we're staring in the rearview mirror. Sometimes, a reset is just what the doctor ordered!

This applies to budgeting, for sure, but it also applies to so many other areas of money and life. We need to stop perpetually beating ourselves up for every mistake and failure, and instead give ourselves a reboot so we can practice excellence in the next season.

Sure, ideally, we wouldn't ever screw up or get behind. In a perfect world, we would continually stay on track forever. We don't live in a perfect world, though. We all live complicated, stressful, busy, and surprising lives. It's almost inevitable that life will kick back at times. When it does, practice the art of the reboot. I hope you find freedom in it. I hope you find relief in it. I hope you find a renewed energy in it.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Messy, But Good

Budgeting is messy! After all, life moves fast.

One of my clients recently lamented how "terrible" their first two months of budgeting were. When I asked what made them so terrible, they said they barely got any categories right and, overall, missed the mark by almost $100. Therefore, in their minds, they failed.

Budgeting is messy! After all, life moves fast. We can have the greatest monthly budget in the world, but the moment a month begins, the world starts spinning. Despite best intentions, things rarely go as planned.

The truth is, even a well-executed budget can be messy. A win isn't defined as nailing every single category and finishing the month at exactly zero. Instead, the goal is to simply do the best we can, knowing we're going to whiff some categories, and get the bottom-line number reasonably close to zero. In my personal budget, I rarely get within $150 of our overall target budget. We regularly miss by hundreds of dollars on either side of the ledger. However, over the years, we have averaged finishing within a few dollars of our target. We care more about getting the long-term average right than obsessing over one specific number.

To give you a real-world example, I thought I'd show what my "successful" March budget looked like. In total, we finished $106 overbudget. Further, it's not as if we nailed every category and just whiffed on one or two; we missed all over the place. Here's what some of our misses looked like on a category-by-category basis:

Home Maintenance: +$50

Kids: -$73

Medical: +$99

Subscriptions: -$124

Hosting: +$51

Other Giving: -$103

We whiffed on six categories by more than $50 and missed our overall budget by more than $100, and that's considered a massive win! Even the best budget can be messy.

Moral of the story: Give yourself grace! If we constantly obsess about getting everything exactly right, we're going to feel like trash. We'll constantly believe we're failing, and after enough failures, we'll just give up. Instead, know that perfection isn't the definition of a win. Get as close as you can, know you'll miss on both sides of the ledger, and trust the process. Ultimately, if we do this, we'll find a healthy and sustainable balance between discipline and grace.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Lessons From the Non-Scam

Money is never about money.....it's always about something bigger. And sometimes, "bigger" means not feeling like our chest is going to get crushed in from the weight of our burdens.

I ate a massive slice of humble pie yesterday, and one of the perks of this blog is that I get to turn my horror stories into writing inspiration (and your entertainment).

While eating lunch yesterday, I received an image from an unknown phone number. No text, just an image. The image was a screenshot of a court date I've apparently been summoned to. Included in the screenshot were a time, a place, and an issue: next week, Chicago, delinquent tolls.

I don't know about you, but for the past 18 months, I've been inundated with scam calls, texts, and e-mails about tolls I allegedly owe. Tolls from states I've never even been to. Needless to say, I ignore every single one of these scammy messages.

Yesterday's random court date screenshot felt different. I wasn't about to scan the QR code in the image, so I found an Illinois DOT phone number to contact. I explained to the agent on the other end of the phone that I think this message is a scam, but I want to check to be sure. She asked for my license plate numbers.

There's a long silence on the other end. At first, I thought we got disconnected. Then, I realized she was processing what she saw and was figuring out how to communicate it to me. "You owe $1,255 in past due tolls."

Excuse me!?!?! After asking several questions, I learned that the original tolls totaled less than $100. However, after YEARS of fees and penalties, I now owe $1,255. Oh, here's the little cherry on top. Since the court date is already scheduled, they aren't willing to negotiate. I was dead in the water. All these years, while I was avoiding the scams, I was simultaneously ignoring real citations. Ouch, just ouch.

Is there a moral to the story? Perhaps the moral of the story is the immense weight I felt yesterday as I was dealing with this mess, and the instant relief I felt when I used the emergency fund to quickly pay for my stupidity. In another place and time, this weight could have sat on me for months.....or years. Some of you know exactly what I'm talking about.

This is one of the reasons why it's so important we get on the positive side of our finances. Money is never about money.....it's always about something bigger. And sometimes, "bigger" means not feeling like our chest is going to get crushed in from the weight of our burdens.

I'm grateful Sarah and I are in a place where we can address this mess without it blowing up our lives. The emergency fund is key. Margin is key. Having no debt is key. Being able to sacrifice is key. All this to say that while yesterday's slice of humble pie hurt, it was a mere bruise compared to what it could have been. Take stock of your financial house, and be prepared for whatever insane storms come your way.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

It Cuts Both Ways

Whenever we think about budgeting, we tend to view it through the lens of "spend less."

Whenever we think about budgeting, we tend to view it through the lens of "spend less." Sure, sometimes that can be true, but that's not the true intent of budgeting. At its best, budgeting is far less about spending less and more about spending better. It's creating a plan, executing said plan, and tracking how we did with said plan.

However, it always seems to come back to the idea that spending less is a win and spending more is a fail. I couldn't disagree more with this sentiment. If a client comes in $1,000 under budget, I tell them they failed. Why? Because they didn't honor their plan. If the plan is to spend $x, they need to spend $x. Therefore, my gauge of how successful someone is with their budget is how close they came to zero. I'd rather someone overspend on their budget by $200 than underspend by $1,000. It's like darts: the closest to the center wins.

Here's how it looks in my household. Last weekend, Sarah asked if we should go out to eat. "Let's look at the budget and find out," I replied. It turns out, for whatever reason, we still had $125 left in our dining out budget for the month. "Let's go out to eat tonight AND tomorrow!" That was great news for us, and the boys were doubly excited.

This is what it looks like to honor a budget. It's not about spending less; it's about spending better. If we negotiate that we are going to spend a certain amount on dining out, then we owe it to ourselves to make good on that promise. We can't blow past that amount, but we also can't fall way short of that amount, either.

It cuts both ways! Think about this idea next month as you create your monthly budget and attempt to execute the plan. Please don't look at your budget as some legalistic, fun-stealing rain cloud that hovers over your life, telling you "no." Instead, use it as the mechanism to bring your goals, aspirations, and motives to life......then live accordingly.

I promise you, if you commit to viewing your money through this it-cuts-both-ways lens, it will change your relationship with personal finance forever.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

A Different Kind of Success

A theme has taken shape in my coaching over the last few weeks. Several families have recently endured a ton of "life." Yeah, let's call it "life." Job losses, medical emergencies, HVAC breakdowns, car problems, unexpected vet bills.....the list goes on. We're talking about thousands or tens of thousands of dollars worth of "life."

A theme has taken shape in my coaching over the last few weeks. Several families have recently endured a ton of "life." Yeah, let's call it "life." Job losses, medical emergencies, HVAC breakdowns, car problems, unexpected vet bills.....the list goes on. We're talking about thousands or tens of thousands of dollars worth of "life."

Needless to say, these couples are discouraged. They had so many goals. Debt payoff goals. Savings goals. Investing goals. Purchase goals. Giving goals. Whatever their goals were, using that money to absorb emergency after emergency wasn't on their wish list.

Despite all that, I view each of these couples as financially successful. Not successful in their established goals, but a different kind of success. In the past, each of these couples would have immediately resorted to debt to pay for these emergencies. The credit cards come out to play. The HELOC takes on a chunk. A new car loan would be in order. Not this time! Today, each of these couples can (and should!) hold their heads high and recognize the fact that they've experienced the brutal realities of life without incurring debt. That's a massive win in my book!!!

I pray each of these families gets back to some form of normal soon, but in the meantime, I will celebrate this massive success of taking multiple punches without punishing their future selves with the burden of debt.

Maybe you're in a season of achieving all the goals you set for yourself. But if not, and like these families, you're experiencing all the bluntness life has to offer, I hope you can create and celebrate a different kind of success. All wins are worth celebrating, even when winning means surviving the onslaught.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

One Number

Whenever someone asks me for financial advice, there's one number I immediately try to get from them to help me understand their approach to life and potential tension level. Want to guess what it is? Nope, not income. Nope, not debt balance. Nope, not retirement portfolio.

Whenever someone asks me for financial advice, there's one number I immediately try to get from them to help me understand their approach to life and potential tension level. Want to guess what it is? Nope, not income. Nope, not debt balance. Nope, not retirement portfolio.

Their house payment as a percentage of their take-home income. Here's an example. If a family has a $2,200 housing payment (rent or mortgage) and a $7,000 take-home income, their number is approximately 31%. For me, that's the magic number. That number alone tells me most of what I need to know.

The higher that number is, the couple has fewer options, less margin, and probably a lot of stress/tension. The lower that number is, the couple has more options, improved margin, and probably a lot less stress/tension. Ideally, this magic number would be less than 25%, but in higher cost-of-living cities, it could be a bit higher.

If I meet with a couple who want to get right with money, but their number is 45%, that's a tough hill to climb. It's going to be awfully tough to pay off debt, set aside money for savings, give, and contribute to retirement. If one single category of life costs almost half of one's take-home income, it puts immense pressure on all the other areas of life. Some would call that being "house poor."

Conversely, if I meet with a different couple who want to get right with money, but their number is 15%, they have a multitude of options! With that level of margin on their largest expense, there's likely money to spare for other, more important categories. Debts can get repaid. Savings can be built. Investments can gain momentum. Generosity can flow. So many options!

I regularly have people tell me that this number isn't a choice. Rather, it's just a reflection of an uncontrollable reality. Never before has that myth been as front and center as it was a few weeks ago, when I met with two couples on the same day. Both couples live in the same town and have similar household incomes (approximately $9,000/month take-home income). One couple's monthly housing payment is $1,800 (20%), and the other's is $4,200 (47%).

Same income, same town! Here's the kicker. The couple with the $4,200 payment, which equates to 47% of their take-home income, was insistent that they are merely a victim of the times. There's nothing they can do to lighten the load, they claim. The other couple, with an $1,800 house payment that accounts for 20% of their take-home income, shared that they intentionally chose to live below their means so they could build a strong financial foundation and follow their callings.

One final thought. Nothing is permanent. If you're in one living situation, there's no law on the books that says you must stay there. Often, this single (weighty) decision can be the inflection point for so much amazing life change. Don't let the world convince you that you're merely a victim of circumstance. Yes, crap happens. Yes, we might be on the receiving end of some negative outcomes. However, that doesn't have to cement your fate.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Perils of Mental Segregation

This is the world's biggest red flag in my book. Whenever we start attributing specific purposes to specific income streams, we've set ourselves up to fail (both financially and relationally).

About six years ago, one of my close friends asked me for some high-level financial advice. As they explained the structure of their household finances, the wife said, "His income is used to pay the bills, and my income is used for travel and fun stuff."

This is the world's biggest red flag in my book. Whenever we start attributing specific purposes to specific income streams, we've set ourselves up to fail (both financially and relationally). No, his income isn't used to pay the bills. No, her income isn't used for travel and fun. Their collective income is used to pay the bills, travel, and do fun things.

Now, you might say that I'm parsing words here, but please track with me for a second. What happens if he loses his job or takes a meaningful pay cut? The weight of keeping the household afloat rests solely on his shoulders. Conversely, what if she loses her job or takes a meaningful pay cut? The weight of the family's financial enjoyment rests solely on her shoulders.

There's one more factor at play. What if she one day desires to stay at home with her kids? They both brushed off that notion, definitively stating that it would never happen. Can you guess where this story is going? Recently, she decided that she has a deep desire to stay at home with their young children. Unfortunately, they never recalibrated their perspective on income allocation, and they are in a bind.

If she quits her job, all wants will be wiped from their budget. Why? "His income is used to pay the bills, and my income is used for travel and fun stuff." They've maintained that mindset up to the present, and it's biting them hard. At some point in the journey, it also transcends from a mindset to an actual reality. If they believe his income is used to pay for the bills (which they have), then they will structure their basic needs to run all the way up to his income. Therefore, there's little margin remaining to absorb the wants if her income decreases.

Tension. Fighting. Tears. Broken dreams. Talks of the D-word. They are in such a tough spot right now, all for something that could have been righted years ago. They specifically asked if I would write about this so "at least some good might come from it." Request granted.

Where do they go from here? In my mind, they have two paths:

She gives up her dream and calling. This option sucks.

They completely recalibrate their view of income. From now on, all there is is money in and money out. "Our income, our expenses." Then, they must make some major sacrifices to free up cashflow on their basic needs (to allow at least a marginal level of wants). This option sucks, too, but they will one day look back and thank their younger selves for doing it.

Please heed their cautionary tale. Any time you find yourself thinking something along the lines of "this income will be used for _____," you're barking up the wrong tree. Instead, add that income to the pot, then make a holistic decision for the entire pot that's best for the family.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Simplify, Simplify, Simplify

One of the biggest myths in the personal finance space is the idea that in order to be financially successful, one must have sophisticated or complex finances. In most cases, the opposite is true. Simple wins.

One of the biggest myths in the personal finance space is the idea that in order to be financially successful, one must have sophisticated or complex finances. In most cases, the opposite is true. Simple wins.

I recently sat down with a couple to help them understand their financial structure. However, it took me a while to understand it before I could even help them understand it. Money was coming and going every which way, and they had bank accounts coming out of their ears. They practically needed a treasure map to adequately interpret the lay of the land.

When I explained to this couple how I structure my personal finances and how I coach other families to do it, they looked shocked. How in the world can it be that simple?!?! After having a similar conversation with two more people yesterday, I thought I'd share it with a wider audience. Want to know just how simple this can be? I'll show you the base structure for day-to-day finances that works fantastically for most couples:

ONE Joint Checking Account. This is the account to which all income flows in, and all expenses flow out. Each person has a debit card tied to this checking account.

ONE Emergency Fund. This is a savings account tied to the above checking account. The purpose of this money is to save us in the event of an emergency. It may not earn much interest, but the money can be accessed at a moment's notice, when life punches.

Sinking Funds. A few named savings accounts are used to save for specific categories. Car, house, travel, and medical are common categories. These are future expenditures that cannot always be absorbed via the monthly budget (such as the $1,600 car repair bill I experienced yesterday). Sinking funds can be housed at the same institution as the two accounts above, but they don't have to be.

That's it. Seriously, if all you have are those accounts, you're positioned to be more successful than 90% of people out there. It's the introduction of credit cards, multiple checking accounts, and random, unpurposeful savings accounts that complicate things. In my professional experience, every layer of complexity that gets stripped away brings people closer to their money.....and ultimately, their goals.

I suspect I'll take some heat for this one, but after working with hundreds of families and diving into the behavioral science of these concepts, I'll die on this hill. Simplify, simplify, simplify. There's no way to outsmart simple. When we spend less time thinking about what goes where and more time on trying to live a meaningful life, the finances become the easiest thing in the world.

You don't have to fully buy into this idea, but I challenge you to simplify one thing in your finances this month. If it makes your life better or easier, simplify one more next month. Repeat. I don't think you'll regret it.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Ridiculous or Not

One of my friends caught wind of something "ridiculous" my wife spent money on. I'm not sure whether he heard it from his wife or from me, but he's right: Sarah's purchase did fall into my definition of "ridiculous." "Why would you let her spend money on x thing that you don't even agree with? I would have just said no."

One of my friends caught wind of something "ridiculous" my wife spent money on. I'm not sure whether he heard it from his wife or from me, but he's right: Sarah's purchase did fall into my definition of "ridiculous."

"Why would you let her spend money on x thing that you don't even agree with? I would have just said no."

Are any spouses seething yet? Good, let the anger soak in for a moment.

Here was my two-fold response:

First, I don't "let" her do anything. Our financial decisions are joint, and she has just as much say as I do. I don't give her an allowance like a child. She negotiates for what she believes is important when we construct our monthly budget.

Which brings me to my second point. If it's important to her, it's important to me......period. Even if I think something is ridiculous (and I often do with Sarah!), that doesn't matter. If it moves the needle for her, I must support her in that. Therefore, when it's important to her, it's important to me. Something fun happens when we take that posture: It gets reciprocated. I promise I spend money on things that Sarah thinks are absolutely ridiculous, too. But just like me, she supports my ridiculousness because it's important to me.

Yes, we should have financial unity in marriage. I'll 100% die on that hill. It's critical to a successful marriage and to successful household finances. That doesn't mean both spouses will value every expenditure equally. Some expenditures will be more your thing, and others will be more your partner's thing. That's okay! That's what makes you a team, and that's what it looks like to sacrifice for each other.

So, yes, I suspect Sarah will continue to desire "ridiculous" purchases. I'll support her every step of the way. If it's important to her, it's important to me.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Allergic to Numbers

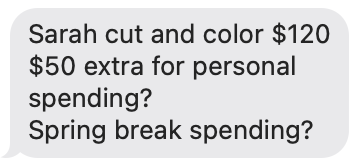

My wife, Sarah, is allergic to numbers. Strange, I know! If it involves numbers, counting, dollars, or math, she's out.

Allergies are common in today's society. Some people are allergic to food. Some people are allergic to pollen. Some people are allergic to medications. My wife, Sarah, is allergic to numbers. Strange, I know! If it involves numbers, counting, dollars, or math, she's out. She's been this way since the day I met her, and I suspect will be the same until the day she dies.

Yesterday, I received the following text from her:

That's right. Numbers. Math. Dollars. This text was her first communication for the negotiation of March's budget. Each month, for the last 200 months, Sarah and I have negotiated a budget for our household. Yes, she's allergic to numbers, but that doesn't exclude her from the process. Yes, I make 99% of our family's income, but that doesn't exclude her from the process. Yes, I'm a professional in this area, but that doesn't exclude her from the process.

I create a draft budget, she reviews it, she provides initial feedback, and then we negotiate. Once the budget is final, we both commit to honoring said budget until the completion of the month. Then, we do it again next month. This is what a team looks like. We each have roles in the process, but we both must be accountable and engaged.

One of my clients recently said they have no idea how they even lived their lives before budgeting became a fixture in their marriage. That resonated with me. If it weren't for Sarah and I's discipline in this area of our lives, there's zero chance we'd be anywhere close to where we are now. Frankly, I'm not sure we'd even have a marriage. The tension that finances have on marriages is massive. In fact, financial tension is the number one cause of divorce in America. That's wild....and sad! My running joke (not joke) with clients is that "Sarah and I have enough issues that we can't afford money to be one of them."

How long does it take me to create the first draft of the budget? Probably 10 minutes. How long does it take for Sarah and me to negotiate the final budget? Probably another 10 minutes. How long does it take me to track our budget each month? Probably 30-40 total minutes throughout the month. Therefore, approximately 60 minutes per month is the difference between living in constant tension, friction, and unknown vs. watching all our dreams come true, with unity.

It's a small price to pay for unquestionable, uncapped upside.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Managing the Puzzle Pieces

Sarah must have picked up on my lack of a good poker face. Translation: I had the look of disgust on my face.

A few days ago, Sarah and the boys came home from a shopping trip. They went to the store to pick up a fun item that, in my opinion, would cost around $25. However, when they came home, they immediately said it had cost $110 instead. Whoa. That's a big delta between expectation and reality.

Sarah must have picked up on my lack of a good poker face. Translation: I had the look of disgust on my face. That wasn't my intention, but the cat was out of the bag. She immediately began throwing out next steps:

Take it back.

Subsidize this unnecessary purchase with her own personal spending money.

Make the kids save up and pay for a portion of it.

I quickly refused all of these options. Instead, I said we should keep this item and manage the monthly Kids spending category accordingly. This purchase, in and of itself, isn't a bad thing. Rather, what happens next will dictate that. That's the beauty of budgeting. Sarah can spend whatever she wants on whatever category she wants......as long as we don't overspend the categories. Therefore, even though she spent a TON on this item, it can still fit within the broader context of our budget. There's a cost. There's a consequence. Perhaps it means not buying the kids a pair of shoes. Perhaps itmeans we do a few less extra treats. Perhaps we go to one less kid's event. It's not about refraining from spending on "wants," but managing the puzzle pieces well.

Every category should be managed this way. Set a dollar amount, then live. Don't guilt yourself. Don't starve yourself of a purchase. Don't live in constant regret. Don't second-guess your partner. Set the budget, then manage the puzzle pieces accordingly. One of the best gifts I can give my wife is to entrust her to manage the pieces however she feels best. I don't question her purchases. I don't criticize her purchases. If she's managing the pieces well and we're staying on track, she's winning; we're winning.

Spouses, this might be what the doctor ordered to reduce financial tension in your marriage. We don't have to look over each other's shoulders. We don't have to question. We don't have to criticize. We don't have to live in fear every time an Amazon box shows up at the door.

Negotiate the budget each month. Set category-by-category targets.

Live your life.

Manage the pieces to fit life within the parameters you set.

Trust each other.

Track your spending along the way.

Know where you landed.

Repeat.

There's a freedom in not having to care about every expenditure our partner makes, trusting that by the end of the month, the targets set in the original budget have been honored.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Little Things Are the Big Things

Despite being a huge Sammy Sosa fan, he always drove me nuts. He wanted to hit a home run on every pitch.

Growing up in the 90s west of Chicago, I was obsessed with the Chicago Cubs. In fact, I made at least one trip to Wrigley Field per year for 20 consecutive years. I love that place. And in the 90s, there was no better place to sit than the right field bleachers. There was nothing like the moment Sammy Sosa made his dramatic run-out to start the game. The fans, including me, would lose their minds.

Despite being a huge Sammy Sosa fan, he always drove me nuts. He wanted to hit a home run on every pitch. Without fail, every single swing was an attempt to club the ball 500 feet, which resulted in so many strikeouts. It's hard to blame him, though, as he was one of the best long-ball hitters ever. However, I couldn't help but think that maybe his swing-for-the-fences-on-every-pitch approach did more harm than good.

A blog reader recently shared a story about how someone in his life wanted “a big plan." Caveat: No budget. A budget is too small. He was looking for something bigger. Budgets are like singles or doubles......he wanted to hit that home run (or maybe a grand slam!).

This resonated with me, as I've seen this play out with clients before. The budget can seem so small, so insignificant. But just like in the case of Sammy Sosa, I can't help but think how much more effective people could be by focusing on the small things, too. I'll take it a step further. Sometimes, the small things are the big things.

A while back, I started working with a couple that made $500,000+ per year. The income was rolling in! When we started working together, they requested that we skip the entire budgeting component of my coaching. And by "requested," I mean they insisted. Reluctantly, but with warning, I obliged.

Fast forward six months, and the couple was displeased with their progress. They set some big goals (home run swings) and went into it with a lot of confidence, yet six months in, they hadn't achieved much (several strikeouts). That's when I reintroduced the budgeting idea to them. In their minds (and words), budgeting was something "poor people had to do." I laughed and explained that not only is budgeting for high earners, but it's actually more important for high earners to budget than lower earners.

Fortunately, and probably for a lack of alternatives, they decided to trust the process for a season. In just the first month, they made more progress toward their very large goal than in the six prior months combined. Why? Because they focused on the little things. Sometimes, the little things are the big things.

I know I beat a dead horse on this topic, but it's so, so important. When we do the small things well, it unlocks the big things. When we focus on getting singles and doubles, we'll score far more runs (and incur far fewer strikeouts) than had we just swung for the fences every pitch.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Our Bellies (and Minds) Deceive Us

When I mentioned the overspending, one spouse jumped in: "What do you mean we overspent on dining out?!?! We hardly ever go out to eat!"

In the middle of a client meeting, I brought up the couple's rampant overspending on dining out. To provide some context, for the past few months, this couple had overspent their monthly dining out budget by hundreds of dollars. In fact, just the prior month, the couple spent $1,000 on this category (vs. their $500 budget). Considering the couple was struggling to meet their financial goals, this category was clearly becoming an elephant in the room. When I mentioned the overspending, one spouse jumped in: "What do you mean we overspent on dining out?!?! We hardly ever go out to eat!"

The second spouse added, "Yeah, we maybe go out to eat once per week. And when we do, it's usually just fast food."

"If that's true, how do you explain the $1,000 you spent last week?" I asked.

"We didn't. No way. Zero chance."

That's when I pulled out the transaction log. 42 transactions were allocated to dining out. I don't know about you, but 42 card swipes at restaurants over a 30-day window doesn't feel like "hardly ever go out to eat."

They were stunned. 42 times!?!? We scanned the list. Yep, yep, yep, yep. All those happened......it just didn't feel like it in the moment. A quick meal here. A pit stop on the way home from practice there. It doesn't take much for a $500 dining out budget to accidentally balloon to $1,000, or $1,500, or even $2,000. The moment we lose intentionality and discipline, all bets are off.

I told this couple not to feel guilty; it happens to the best of us! I think we've all been there before. The important part isn't feeling bad about it, but rather developing an awareness of our gaps.

Want to know what happened next? The couple became quite aware of their dining out spending. Month after month, they locked in on the desired number. With fewer trips out to eat, they made sure to enjoy them more. They chose wisely, carefully. And they started meeting some of their other financial goals! Huge win!

Our bellies (and our minds) can deceive us. I'm the world's biggest fan of dining out, but we must be intentional and practice discipline. The same goes for all the areas in our monthly budget. It's never about spending less, but spending better. Find your better.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

A Question From Mr. Clear

We need to lean harder into the things that add value to our lives while simultaneously turning our backs on the things that don't. That's the recipe for finding more meaning in our money.

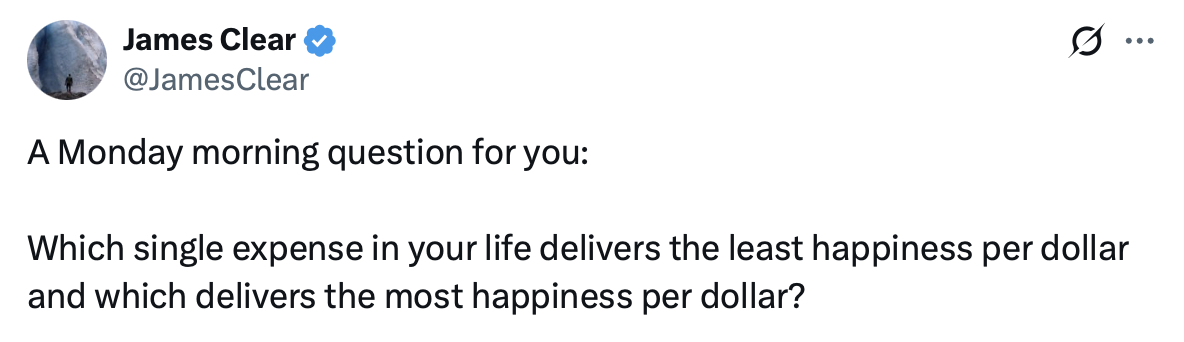

In doing some research for a potential project, I stumbled upon a Tweet yesterday afternoon. James Clear, the author of the best-selling phenomenon book, Atomic Habits, asked a profoundly meaty question:

This falls in line with my ongoing messaging about budgeting: "It's not about spending less, but rather spending better." We need to lean harder into the things that add value to our lives while simultaneously turning our backs on the things that don't. That's the recipe for finding more meaning in our money.

When I see families exhausted and frustrated by their finances, it almost always includes their unintentional spending on things that don't actually matter to them. Consequently, they don't have the resources to spend on things they actually care about. It's the ultimate emotional drain.

However, when we can be laser-focused on what actually matters to us, blocking out all the noise around us, it oftentimes feels like we got a raise. Further, life just feels better when our resources go toward valuable things. There's no worse feeling than spinning our tires by spending all our hard-earned income on stuff that doesn't move the needle in our lives.

I'll answer Mr. Clear's questions, but after I do, I challenge you to answer them for yourself.

What single expense in my life delivers the least amount of happiness per dollar spent?

This might be an unpopular opinion in my house, but some of our streaming services. If it were up to me, we'd justhave YouTubeTV and Netflix.....that's it. However, because x show is on y platform, we subscribe to y platform. And z show is on b platform, we subscribe to b platform. In my mind, this is one of the least effective categories in our budget.

If this is true, I should probably engage Sarah about this and see how important it is to her (and how important it is for me to push back on).

What single expense in my life delivers the most amount of happiness per dollar spent?

Dining out, and there's not a close second. I so cherish the time our family spends dining out, whether it's a quick meal with the kids or a date night with Sarah.

The other one I was debating was Travel, but on a dollar-for-dollar basis, dining out offers a far higher return.

If this is true, it would argue that we should consider increasing our dining out category each month. I think we skimp on this one far too often.

Your turn.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

100% Ours

Tempers were flaring, f-bombs were tossed like hand grenades, and the occasional tears arose. This was the scene of a recent sit-down I had with a struggling couple.

Tempers were flaring, f-bombs were tossed like hand grenades, and the occasional tears arose. This was the scene of a recent sit-down I had with a struggling couple. The subject matter: the income differential between the two spouses. More specifically, how the couple makes financial decisions given their income differential.

Here's the high-level summary of the situation:

Husband makes 70% of the income, and the wife makes 30%.

The husband handles the day-to-day finances.

The husband's income pays for the family's needs, and the wife's income pays for the wants (travel, dining out, entertainment, etc.).

The husband spends anything he wants, but gives his wife "an allowance." After all, she only makes 30% of the family's income.....so this is generous (his words, not mine).

Every time there's an argument, the husband throws out the trump card: "I make more than twice as much as you, so I get to make the call."

As the conversation unfolded, the husband realized I must have had a look of disgust on my face at the words coming out of his mouth. He seemed surprised. After all, he knew that I was the breadwinner in my marriage. As such, I would naturally align with him, right?

By my records, I made 98.5% of our family's income in 2025. Translation: My marriage is far more unbalanced than his. With that context in mind, I explained to them (mostly him) that their way of handling finances is beyond toxic. They are keeping score with money and using it as a weapon. Further, their dumb idea of allocating her income to wants meant that if she ever wanted to take a different job or stay at home, she would be solely responsible for ripping all enjoyment and adventure from the family. Gross.

I may make 98.5% of my family's income, but our income is 100% "ours." Not mine. Not mostly mine. Ours. Everything Sarah and I make is viewed as a collective pot for us to manage together. Yes, I do the day-to-day finances. Yes, I createthe first draft of the monthly budget. Yes, I have more financial expertise than her. However, she ALWAYS has a 50/50 say in all we do. In fact, early in my marriage, I promised myself that I would never get more monthly personal spending money than she does. She would always get the same as me....or more on some occasions.

Something powerful happens when couples view money as a collective pot. It allows a full integration of life and decision-making. This income isn't for this, and that income isn't for that. It's just money in and money out. We're both called to different work in our lives, and in this season, my work provides 98.5% of our income. That doesn't make her less valuable or less impactful. It just means my work pays more. Sarah is impacting the world in different ways; important ways.

Whatever income dynamic you have in your marriage, I strongly (STRONGLY!!!) encourage you to adopt a "100% ours" mentality. You're a team, not a competition. Be in this together, side by side.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Under Our Noses

Do you ever feel like you don't have much, if any, financial margin in your month-to-month life?

Do you ever feel like you don't have much, if any, financial margin in your month-to-month life? I've felt that way at times, and I regularly meet people who believe the same.

I could tell countless stories about this idea, but instead, I'll share one specific encounter I recently had that perfectly sums up today's point. Here's the context:

Husband and wife, both late 30s.

Three young children.

Monthly take-home income of around $9,000.

They have a mortgage and one medium-sized car loan.

Constant frustration and tension in the marriage since there isn't margin to do the things they really care about.

We spent about an hour going through their budget. Sure enough, there really isn't any margin once everything is accounted for. Or is there?

What I often find is that even when people don't believe they have margin, they actually do have margin right under their noses. It's sneaky. Category by category, I whiteboarded all the components of margin I saw in their financial life.

$800 worth of dining out each month.

$175 worth of streaming services each month.

$500 worth of combined personal spending each month.

$500-$750 worth of travel each month.

So while finances feel tight and there doesn't appear to be margin, they DO have margin. However, they've just chosen (whether consciously or subconsciously) to use that margin to fill the above-referenced categories. In total, they had approximately $2,200/month of actual margin.

My challenge to them was to look in the mirror and sincerely ask themselves what they wanted to do with that margin. It's okay to do what they are already doing, but it's not okay to whine about it and feel like a victim. If they are a victim of anything, it's of their own choices. Therefore, let's make sure we're making rock-solid choices.

I didn't share this with them to guilt them or embarrass them. Rather, I wanted them to see just how truly blessed they are. Second, I wanted them to embrace this opportunity to add the most value to their lives.

After multiple conversations, they reoriented where some of their monthly cashflow was going. This month, they don't feel nearly as stressed. They don't feel like victims. They don't feel like they are on the outside of their dreams, looking in. They recognize the margin they do have, and they are embracing the opportunity to harness it well. Beautiful!

It's a fantastic exercise. I encourage you to try it for yourself!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Life Happens

Wanna know how often a typical family's monthly budget goes exactly as planned? Maybe 10% of the time if I'm being honest.

Wanna know how often a typical family's monthly budget goes exactly as planned? Maybe 10% of the time if I'm being honest. This is a conversation I frequently have with clients as they begin their budgeting journey. There's usually this moment within the first few months of the process where my client feels defeated; a failure of sorts. In their mind, a budgeting win means that every category gets nailed right on the head.

Life doesn't happen on paper, unfortunately. It's messy. It's sudden. It's imperfect. We can have the world's best budget to start the month, but life has other plans. Success doesn't mean nailing the budget just as we've outlined it. Rather, success is our ability to track, be aware of our changing reality it in real-time, and make the necessary adjustments along the way to account for life happening in hopes of landing on even footing by the time the month concludes.

This month is a great example for my household. Due to my back injury, we're going to face significantly more out-of-pocket medical expenses than planned. Given the stress we've been under, we'll likely also blow past our planned dining out budget. Now, we can't just throw our arms up in the air and play the victim card; nobody wins under that scenario. Instead, we must take accountability for the life that's happening, first by being fully aware of its impact, and second by making the necessary adjustments.

What this looks like for Sarah and me is a combination of things:

A reallocation of the dollars we had already planned to spend. Some of our discretionary spending will be reallocated to the increased categories. We may also temporarily reduce the recurring savings we push toward a few of our sinking funds.

An additional allocation of funds from emergency savings. We don't typically touch our emergency fund (that's why it's called an emergency fund), but that's what it's for. It exists for exactly this purpose.

A deferral of a few other priorities. There are some decently important obligations in our lives, but for at least this month, those priorities must move down the list.

These newfound expenses don't deem December a failed month for us, but how we respond will. It's not ideal, and it's tremendously frustrating, but that's life. Life happens. Life always happens. It's just our job to adapt along the way.

Whether you're having the world's best budgeting month, or the worst, success or failure isn't determined until you decide how to handle it. It'll never be perfect, but you don't have to give up control.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.