The Daily Meaning

Take your mornings to the next level with a daily dose of perspective and encouragement to start your day off right. Sign-up for a free, short-form blog delivered to your inbox each morning, 7 days per week. Some days we talk about money, but usually not. We believe you’ll take away something valuable to help you on your journey. Sign up to join the hundreds of people who read Travis’s blog each morning.

Archive

- August 2026

- July 2026

- June 2026

- May 2026

- April 2026

- March 2026

- February 2026

- January 2026

- December 2025

- November 2025

- October 2025

- September 2025

- August 2025

- July 2025

- June 2025

- May 2025

- April 2025

- March 2025

- February 2025

- January 2025

- December 2024

- November 2024

- October 2024

- September 2024

- August 2024

- July 2024

- June 2024

- May 2024

- April 2024

- March 2024

- February 2024

- January 2024

- December 2023

- November 2023

- October 2023

- September 2023

- August 2023

- July 2023

- June 2023

- May 2023

- April 2023

- March 2023

- February 2023

- January 2023

- December 2022

- November 2022

- August 2021

- November 2020

- July 2020

- June 2020

- April 2020

- March 2020

- February 2020

- October 2019

- September 2019

The Moment I Knew

"While we're on the road, the two people who aren't driving spend time contacting and pitching everyone. Old clients, warm prospects, cold prospects.....everyone."

One of my commercial clients is comprised of three young, talented, hungry owners. They are brilliant at their craft, but not accomplished business owners.....yet. In the midst of trying to grow their newish business, they lost a key client. Many of their aspirations for near-term growth skidded to a halt, replaced by a sudden need to piece together a few deals to stay afloat.

One of them recently reached out with a question. I immediately called them back and happened to catch them while they were driving across the state for a work project. One of the owners said something to me that quickly caught my attention. They recently purchased a mobile Starlink unit so they have high-speed internet in their vehicle on road trips. Why? "While we're on the road, the two people who aren't driving spend time contacting and pitching everyone. Old clients, warm prospects, cold prospects.....everyone."

That's the moment I knew they were going to be just fine. Being brilliant at our craft isn't enough. Often, it takes a mastery of our craft combined with a relentlessness and humility to just go for it. What makes these three individuals unique is that they are impervious to failure. They could have 1,000 doors violently slam in their face, only to knock on the 1,001st door with full confidence that it will be a "yes."

I wish I had that same relentlessness gear they do. I've been thinking a lot about that conversation, and it's forced me to look in the mirror with my own attitude and approach. For as successful as I feel like I've been, I can't help but wonder what things would look like if I developed a gear like these three have. It's an interesting thought experiment, and it pushes me out of my comfort zone. Maybe you need a similar nudge today. A nudge to develop a relentlessness and motor to keep going, regardless of how many shut doors you encounter. Something to think about as you go about your day. Have an awesome one!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Chicken or Egg?

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?"

I recently stumbled upon a heated online conversation on a social media platform. The original poster posed a question: "If so many people are struggling right now, why are there so many people with brand-new vehicles parked in their driveways?" It seemed counterintuitive, as these new vehicles are presumably evidence that people are doing well.

Let's just say the comments were lively. Hundreds of people chimed in, positively confirming that most people are, in fact, doing great. The commenters believed they, individually, were simply part of the small share of people who are struggling, while everyone else is thriving.

I have news to break to them (and anyone else who will listen). Those brand-new vehicles sitting in people's driveways aren't evidence that people are doing great. Rather, those same vehicles are one of the primary culprits for why people are struggling so much. People's vehicles are putting them into a financial grave, month after month.

I recently met with a successful-looking couple who, from the outside, appear to have it all put together. They are fit, their kids are cute, their house is immaculate, they have good jobs, and they both drive new vehicles. The subject of the conversation? How they can stay financially afloat and not lose everything. Truth be told, their monthly finances didn't contain many red flags. Lots of normal, but not outlandish spending allocations. However, there were two major red flags.....and both were parked in their garage:

His vehicle: $1,100/month payment

Her vehicle: $850/month payment

Total vehicle payments of $1,950. In my brain, that's called a mortgage payment. Two thousand bucks for vehicles!?!? Both assured me that 1) they can afford them, 2) they are perfectly reasonable vehicles, and 3) everyone else has at least as nice vehicles as they do.

They aren't alone. This is a dynamic I see every single week in my coaching work. I've met with hundreds of families, and vehicle tension is the leading contributor to financial pain, suffering, tension, stress, and destruction. Not a lack of income, student loan debt, a failure to budget, or limited financial literacy. Vehicles. Vehicles are literally milking an entire society dry.

Many people who read this piece will roll their eyes at me. This topic often draws the ire of those who digest my content daily. That's okay, though, as this message needs to be shared over and over and over. I so badly want people to live a quality of life, and if I can get them to make different decisions in this vehicle department, I strongly believe it will have a direct positive impact on their quality of life.

We need more humility. We need more patience. We need to care a whole lot less about what others think. That's the ticket to some beautiful things in our lives. Please don't allow a vehicle to play a significant role in your journey. It can play a role, but not a leading role. You deserve better; much, much better!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Outgrowing Your Structure

I recently met with a couple who are becoming progressively more frustrated with their finances. This seems counterintuitive, though, as they are making far more money than they ever have before. Why, then, are they getting frustrated? It's pretty simple: The current complexity of their life has outgrown their financial structure.

I recently met with a couple who are becoming progressively more frustrated with their finances. This seems counterintuitive, though, as they are making far more money than they ever have before. Why, then, are they getting frustrated? It's pretty simple: The current complexity of their life has outgrown their financial structure.

Translation: The way they used to handle finances worked well then, but not so much anymore. It was easy to wing it and be more casual when there was less income and fewer obligations. However, life is getting more complicated, and the old way of doing things seems inadequate at best, destructive at worst.

It reminds me of a similar situation we're having at Northern Vessel. Nearly four years in, it's safe to say our business looks a little different than it once did. During a recent team dinner (celebrating one of our team members who left to pursue a new dream), it was time to pay the bill. TJ couldn't be there, so it was on me to pay. Unfortunately, I forgot to ask TJ for the debit card. At the last second, Jack swooped in to pay the bill, somehow having TJ's card in his wallet.

That's right, we literally have only one debit card. The entire company has been operating with one debit card and one checkbook. We have tens of thousands of dollars in monthly expenses, yet the entire operation rests on one debit card and one checkbook. We've outgrown our structure, and we're experiencing the consequences.

Whether it's the family I mentioned above or a company like Northern Vessel, we must iterate on the structure as we grow. What once worked might not be adequate in the new season of being. Taking the "this is the way we've always done it" approach is a surefire way to end up in a bad place. Therefore, we need to give ourselves permission to evolve, adjust, and continue to find better ways to handle ourselves.

Some of you are handling your family's finances the same way you did when you were young, single, broke, and fresh out of college. Except now, you have a spouse, kids, a house, and multiple incomes. It might be time to update the structure! For some of you, simply upgrading the way you do things might be the ticket to significantly better outcomes. It doesn't matter if you've done it the same way for 20 years.....it might be time to adjust.

Never be scared to make changes. As life becomes more complicated, find ways to simplify and find order amidst the chaos. You'll thank yourself later!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

What’s Your Weird?

People frequently tell me that I'm "weird" in how I spend money.

People frequently tell me that I'm "weird" in how I spend money. I never take offense to these comments. In fact, I love them! I wear them as a badge of honor, and in some ways, they tell me I'm right where I need to be. Here are some examples of things people have told me I'm weird for doing:

When it comes to my personal residence, I'm a perpetual renter. I've owned two houses in my adult life, but I much prefer renting over owning.

The biggest category in our household budget is giving. This is non-negotiable.

Our second-largest category is travel. This is also a non-negotiable.

I will gleefully spend a few hundred dollars on a first-class meal. I've had $25 dinners that felt expensive and $250 dinners that felt cheap. An amazing meal is worth its weight in gold.

There's no amount of money too much when it comes to creating once-in-a-lifetime memories.

When I'm at a coffee shop, restaurant, or bar with someone, I almost always offer to pay for them.

If someone offers to buy my coffee, meal, or drink, I accept.....always. No exceptions.

When eating at a sit-down restaurant, the minimum I’ll tip is 20%, but it’s usually closer to 40%-50% if the server demonstrates excellence. It’s one of the few areas of life where people will gratefully accept generosity, so I love to lean into it as much as possible.

I will never purchase a new vehicle. In fact, I've never purchased a new vehicle. At best, any vehicle I purchase is probably at least 3-4 years old.

I will always pay for services that save me time, sanity, or stress.

What say you? Do you find these weird? I hope so, as you're different than me. That's what makes this money stuff so fascinating. We're all wired differently, heavily influenced by our experiences, values, upbringing, and circumstances.

I want to know what weird money habits you have. Please hit reply to this e-mail if you're a subscriber, or comment below if you're on the website. Please share your quirks with me. If enough people reply, I'll put together a fun little list and share it in a future post. Have an awesome (and weird!) day.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

There Are No Secrets

The secret is there are no secrets.

After a recent public speaking engagement, during the customary Q&A session, someone asked an interesting question: "I heard you've written and published your writing more than twelve hundred days in a row. First, is that true? If so, what are your secrets?"

Every day since November 14th, 2022. Pushing nearly 1,400 days now. It hurts my head to think about that. It doesn't feel real; it doesn't feel possible.

The secret is there are no secrets. As I've learned about writing, and the same goes for almost any discipline, the only way to write is to write. The only way to publish is to publish. What is required of me is to sit down in front of a screen and create.

Follow-up question: "Do you write a bunch at once and batch it for the next several days?"

No batching. One piece of writing per day, every day, no exceptions. There's something wild that happens inside us when we eliminate the excuses and just commit to the craft. It strips away any and all shortcuts and shortcircuits that could potentially sabotage the habits we're trying to create. I write because I write because I write. At some point, these habits become as normalized and as common as brushing our teeth or tying our shoes. It's just what we do.

Here's another way to think about it, back to my comment above about how it doesn't feel real or possible to write nearly 1,400 days in a row. The good news is I didn't have to write 1,400 pieces. I just had to write one. Then another one. Then another. I'm writing one today. Then tomorrow, I'll write one, too. The only one that matters is the next one. There's a freedom in that! Whatever we're trying to accomplish, just worry about the next one. After that one is done, we can worry about what lies on the other side of that one.

So many people have so many dreams. But those dreams seem daunting, maybe even impossible. You don't need to accomplish all those dreams in one fell swoop. You only need to accomplish the next thing that's sitting in front of you. Then, move on to the next.

I recently had a buddy run a marathon. Running 26.2 miles boggles my mind, so I asked him how he approaches it. "It usually takes me about 40,000 steps to complete it. It's too overwhelming to think about 40,000 steps, so I just try to focus on the next step. If I can stay focused and use good technique for the next step, eventually, the next step will be the 40,000th step. It just kinda happens."

The next step. The next step is all that matters. That's the secret. There are no secrets. Just one foot in front of the other, whether literally or figuratively. Have a great day!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Want-to-Need Migration

Much discourse centers around the idea that life is so much more expensive today than it used to be. We blame inflation, capitalism, Boomers, politicians, and the systemic structure of our modern-day society.

Much discourse centers around the idea that life is so much more expensive today than it used to be. We blame inflation, capitalism, Boomers, politicians, and the systemic structure of our modern-day society. In other words, we love to blame everyone except the person in the mirror. Has life gotten more expensive? Sure. It always does. That's how inflation and the time value of money work. In all of this discourse, I think we've missed the biggest culprit of all: the want-to-need migration.

Over the past 25 years, I've personally witnessed a slow and steady cultural shift from what was once a want to now a need. Houses are a great example. When I was a kid, young families lived in small, conservative houses. However, over time, the average square footage of houses in America grew, as did the expectations of younger homeowners. Houses we now consider "starter homes" would have been mini-mansions 25 years ago. What about those small, conservative houses people used to live in? It would be unthinkable to live there!!!! Out of the question! Our expectations for the houses we choose have migrated from a want to a need.

Dining out is another great example. I recently met with a family who said a $600/month dining out budget is a "need." They didn't want a $600 dining out budget; it was a basic human need for their survival. Conversely, 30 years ago, dining out was more of a luxury. In my house, it felt more like a twice-per-month event. Taco Bell was a treat, Pizza Hut was a splurge, and Golden Corral was fancy. Our dining out habits have migrated from a want to a need.

Off the top of my head, I can think of countless items we now call needs that would have been wants 20+ years ago, including:

Streaming services (many people didn't even have basic cable in the 80s and 90s).

Cell phones (not in most people's budgets).

Internet service (also scarce).

Plane tickets (air travel used to be rare; today it's the norm).

Coffee shops (as the 90s kids ask, "What's a coffee shop and why would anyone go there?")

Online shopping (it was much harder to spend money in the pre-internet days, when you used to have to drive to the store. Today, click, click, click....delivery in an hour).

I'm not saying there's anything wrong here. In fact, I enjoy all of those things I just listed. They are part of my budget and part of my family's rhythm of life. I'm grateful for them. However, we ought not forget what's really a need and what's really a want. Sometimes, we need to get back to basics: food, clothing, transportation, and shelter. Let our needs be needs, then address our needs head-on. Once we've accomplished that, then we can move on to the wants. But let's let wants be wants. View them as such. Treat them as such. Enjoy them as such. Don't let your wants migrate into needs.....that's the gateway drug to much stress and bad outcomes.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Exhibit #975

I recently stumbled upon a social media video in which a woman asked, "If you were offered a free vacation, but you weren't allowed to post any photos of the vacation on social media, would you still go?"

I talk often about the hidden psychological forces that influence our daily habits and decision-making. These hidden forces play a much larger role in our lives than we'd like to admit, and most people won't admit it. Today, I'd like to talk about Exhibit #975. Is it really #975? Not sure....I'm just guessing at this point!

I recently stumbled upon a social media video in which a woman asked, "If you were offered a free vacation, but you weren't allowed to post any photos of the vacation on social media, would you still go?" She continued by saying that she would feel that a trip without social media photos would be "a waste," and thus would decline.

My first reaction to her question was, "Of course I’d go! In fact, I'd prefer not to share a single photo of my trip! Double win!"

I saw lots of similar remarks in her comments. However, the vast majority of people agreed with her. If you can't post photos of your trip on social media, what's the point? Thousands of people chimed in, arguing that there's not much of a point in going on a vacation if you can't share content from it. Many people said they'd rather pay to go on the same trip so they can post whatever they want.

Depending on the study, 45%-55% of Millennials and Gen Z care about their vacations looking good on social media. Some even select their travel destinations solely for the aesthetics of the soon-to-be social media posts. In other surveys, approximately 20% of people admit to posting photos to boast, while another 10% admit to posting photos to incite jealousy from their friends, family, and colleagues. Here’s another fun one. 75% of people say they get annoyed when friends and family post vacation photos, yet even so, 75% of those annoyed people will do the same by posting their own photos. It’s a social media arms race of vacation photos!

We, humans, are a weird bunch. Now, regardless of what side of the aisle you land on with this question, this is another piece of evidence illustrating just how much we're being influenced by culture. You and I might not be struck by this particular ridiculous affliction, but we're struck by some other, equally ridiculous afflictions. Somewhere, deep down in our psyche, we're being manipulated by a combination of our culture and our subconscious.

Maybe it's the vehicles we're buying. Maybe it's the houses we're living in. Maybe it's the clothes we're wearing. Maybe it's the clubs we're joining. Maybe it's the technology we're using. I'm not suggesting that we ought to stop being impacted by these forces. If we're human, it's inescapable. Instead, what I'm suggesting is that we become aware of it in our own lives. Once we have awareness, we can take it into account in our decision-making process and make better choices.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

If Everything Is Important…..

Here's a general truth. If everything is important, nothing is important.

I received a half-dozen messages yesterday in defense of the family I discussed in yesterday’s post. In short, people defended this family's actions by saying that all of these things were important. Thus, this family was simply a victim of having all these important things stacked on them.

Here's a general truth. If everything is important, nothing is important. Let's say there are 50 different things vying for our time or money, and all of them are deemed "important." If they all occupy the same plane of importance, then none of them are actually important. In a world of relativity, none of them win.

This is the curse that strikes so many of us. Our budgets are living testimonies of this. For example, I'll regularly meet people who are actively saving for 15 different things—$ 25 here, $30 there. When I do the math, I point out to them that it will take years to knock out any of them. That becomes immensely frustrating, eventually defeating.

For this reason, we need to truly prioritize. Are some of these things in our lives needs and wants? Yes. That's totally cool. Allow them to live in our hearts and minds. However, we need to be honest with ourselves when setting priorities. Once we have our list of upcoming needs and wants, do whatever it takes to prioritize them so your values can be lived out.

If everything is important, nothing is important. Therefore, keep it simple, prioritize, and execute. Confidently knock out the most important goal, then move on to the next.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Don’t Let the Sequence Fool You

This young guy fell into the same trap so many do. Instead of viewing his money as a giant puzzle, he viewed it as a sequence of transactions.

A young man asked me to look over his finances and help him get some control. Included in this conversation was a review of his most recent bank statement.

"Dude, you spent $700 more than you made last month!" I exclaimed.

"I had to buy groceries at the end of the month. What, you expect me just not to eat?"

"No, I expect you not to implode your finances by plunging yourself into debt."

"I had no choice, Travis! Either I buy groceries, or I don't eat."

"The sequence of your purchases isn't what matters here. That $700 of overspend doesn't just get credited to the last $700 you spent in the month."

"Again, I HAD to buy groceries."

"Did you need the other $1,200 of impulse purchases you made before that?"

“……….”

This young guy fell into the same trap so many do. Instead of viewing his money as a giant puzzle, he viewed it as a sequence of transactions. Then, when he had known and tangible needs, he acted (even though he had already exceeded his budgeted income for the month). This is how we end up in debt. This is how we never have funds for wants. This is how we can't afford to invest. This is how we justify not giving. We spend, spend, spend, then when a NEED arises, we flippantly meet that need without regard for the consequences.

It's a psychological phenomenon that often strikes us humans. If you're human, you're subject to it. What's the solution? Have a plan for the month. The WHOLE month. We know we need groceries. We know the rent or mortgage has to get paid. We know we'll need to put fuel in the vehicles. These are known expenses. Therefore, plan accordingly. While we're planning, we should also plan for the fun stuff. Plan for the dining out. Plan for the date nights. Plan for the concerts. Plan for the plane tickets. Plan for the new clothing. The keyword is "plan."

Let's remove the bias toward sequence and replace it with a bias toward intentionality. Oh, you really, really want a new Blackstone grill? Great! Is it in your plan? If not, then don't do it. Put it in your plan next month. Then buy it! The goal here isn't to demonize spending, but to demonize unplanned, impulsive, destructive spending. Let your plan be your plan, then execute. If it includes a fun trip or a Blackstone grill, go for it! But we can't constantly buy things that aren't in the plan, blow past our budget on buying true needs, then blame the needs.

We can do better! We deserve better. We'll thank ourselves for giving ourselves better!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Mazzulla Has a Good Point

But then, there's Joe's perspective. Man, we're so blessed. Most of us will wake up today more blessed than the vast majority of people who have ever lived on this planet.

I recently stumbled upon an interesting video clip of Joe Mazzulla. Joe Mazzulla is the head coach of the Boston Celtics, known for his sharp comments to the press. Sometimes, his responses seem a bit unreasonable and impatient. However, there are times when he responds in profound and thoughtful ways. Today's video clip is of the latter.

Reporter (asking Joe about how he's dealing with the brutally difficult stretch his team is going through): "Is there something you're doing in the last 48 hours to keep yourself away from just being consumed with this? Are you watching different movies?"

Joe (with a shocked look on his face): "Honestly, I met three girls under the age of 21 with terminal cancer. I thought I was helping them by talking to them, and they were helping me. And so having an understanding about what life is really all about, and watching a girl dying, and smiling, and enjoying her life.....that's what it's really all about. And having that faith. You know, the other thing is you always hear people give glory to God and say thank you when they're holding a trophy. But you never really hear it in times like this. And so for me, it's an opportunity to just sit right where I'm at and just be faithful. That's what it's about."

Perspective matters. We need to remember what's really important as we live our days. It's so easy to get caught up in the small, ultimately meaningless nuances of life. The person in front of us didn't accelerate when the light turned green. Someone at the coffee shop cut in front of us in the line. Our co-worker gave us a snooty attitude when we asked for a favor. One of those dumb speed cameras caught us going 57 in a 45, and now we must send some rando a $97 fine. We didn’t get the promotion we so desperately wanted.

But then, there's Joe's perspective. Man, we're so blessed. Most of us will wake up today more blessed than the vast majority of people who have ever lived on this planet. Yet, many of us will wallow in self-pity and frustration today, looking for reasons to feel negative about the journey. We lose perspective.

I hope you live today knowing just how blessed you are. Not a perfect life. Not a life void of baggage, pain, and suffering. But blessed nonetheless. Remembering that fact has the potential to re-frame our entire day, allowing us to focus less on ourselves and more on others. That's the ticket to meaning and impact.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

A Middle Finger To Our Future Selves

To his detriment, he lived out the principles he preached way back then. He spent, spent, and spent, giving little regard for his future self.

I remember speaking to a colleague nearly 20 years ago. He was probably in his early 30s at the time, several years ahead of me in his career. While I wasn't necessarily the wisest steward with my financial resources back then, he and I shared many conversations that stopped me in my tracks. These conversations usually centered on the idea that we don't know whether we'll even be alive when we're older, so we might as well "enjoy life" while we're young. And by "enjoy life," he meant spend, spend, spend. He hated the idea of saving, or heaven forbid, investing. If he had it, he was going to blow it on something fun.

Fast forward 20 years, and I recently ran into him. He's now in his 50s, visibly older than when we last connected (as a few decades of life will do). This time, though, his attitude was different. He was asking me about retirement, investing ideas, and the worry about likely not having enough.

To his detriment, he lived out the principles he preached way back then. He spent, spent, and spent, giving little regard for his future self. In fact, I'd argue he gave his future self a hefty middle finger. It turns out, though, that one day, our present self becomes that future self. Today, he's the future self that younger him so blatantly disrespected.

He's scared....as he should be. His options are limited.....as expected. He feels trapped.....which is understandable. Now, his 50-something self is wondering how to navigate not only the present, but the future. He lived a lot of life in his younger days, but his current and future quality of life are very much in question.

This is a tough situation. I have so much empathy for people who face these realities. Unfortunately, I don't have a magic wand to wave for them. I can't undo their past mistakes. There's no magic pill or secret strategy to bridge decades of gaps.

No matter how old you are today, future you is depending on current you to make wise choices. Sacrificial choices. Loving choices. Be a good steward, not only with your finances, but with your body, relationships, children, marriage, and mental health. Future us is pleading for us to be better and do better. Their livelihood depends on it, and soon enough, that will be our present self. Be good to him/her.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Two Families, Two Perspectives

I had a few interesting conversations last week that showcase an important concept. It's about two different families. Both families live in the same town. Both families have two kids under the age of 12.

I had a few interesting conversations last week that showcase an important concept. It's about two different families. Both families live in the same town. Both families have two kids under the age of 12.

Family 1:

The husband has a monthly take-home income of approximately $10,000.

The wife has a monthly take-home income of approximately $5,000

The total monthly take-home income is about $15,000

This family endures constant financial stress. There's rarely anything left over. The credit cards often come out to play. Most purchases are made with debt. There's very little savings, and giving seems like a pipe dream. Marital tensions are running high. Their overall sentiment is that if they just made a little more money, all of this financial stress would go away.

Family 2:

The husband has a monthly take-home income of approximately $5,000.

The wife stays at home with their two small children.

The total monthly take-home income is about $5,000.

This family's entire monthly income stream approximates the lower-income earner in Family 1. Their total take-home income is 1/3 of the other family's! Yet, they don't feel financial stress. No, there isn't a ton of extra each month, and they need to be diligent with the dollars they do have, but life is good! They consider themselves blessed, save for the future, and ensure giving is part of their monthly rhythm.

Would more money help? Yeah, it probably would. However, more isn't the answer. More isn't what defines our success. More isn't some magic pill that solves all of life's problems. This is a phenomenon I see over and over. Yes, more income can help, but 90% of our problems are the person staring back at us in the mirror, not the dollar amount on our paycheck. The sooner we realize this, the sooner we can take steps actually to improve our quality of life.

Final thought. Just imagine if we could do both. First, we get right with our relationship with money. We have a healthy mindset. We establish solid practices. We make the best use of every dollar we're blessed with.

Then, second, we find ways to increase our income along the way. We put in the work. We practice excellence. We pay our dues. We meet people's needs. We add value to the organization. When we do these things, additional income is a natural byproduct.

Combining these two ideas can literally revolutionize our lives. When we get right with money and put in the work, it's amazing what can happen!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Once You See It

Something powerful happens when we see parts of the world that are extremely foreign to us. When we leave our little bubble and get a glimpse of the bigger picture, it has the potential to melt our minds. Everything we know and believe can be turned upside down in a matter of days.

I recently found out that one of my friends is taking her family abroad this summer. Not some fancy adventure to Europe, but a deeply cultural experience in a place most Americans will ever see. "This will change your kids' lives forever!" I exclaimed. She wholeheartedly agreed.

Something powerful happens when we see parts of the world that are extremely foreign to us. When we leave our little bubble and get a glimpse of the bigger picture, it has the potential to melt our minds. Everything we know and believe can be turned upside down in a matter of days.

I didn't have one of these experiences until my 30s, but when I did, it permanently shifted my life forever. It's one of the reasons my family lives in a one-bathroom house and drives aging vehicles. No matter how we live here in our bubble, we're rich. Period. There's no way around it. Once you see it, you can't unsee it.

People are hurting. People are sick. People are hungry. People are cold. People are hot. People are unsafe. Yet, here we are, whining that our house isn't big enough, our cars not new enough, our clothes not sylish enough, and our technology not fast enough.

Here's a thought that often crosses my mind. If I had the choice between improving my family's standard of living and helping hundreds (possibly thousands) of people attain a livable standard of living, which would I choose? It turns out, we have that choice every day of our lives. It's easy to think we don't actually make that choice, but not making a choice is still making a choice.

This isn't meant to elicit guilt. Guilt is a terrible master. Rather, this is my encouragement for each family to seek out new perspectives. Let's step out of our bubbles and truly see what's going on around us. Let's get uncomfortable. Let's challenge ourselves to open our eyes. Let's get an up-close view of how the rest of the world lives. Then, and only then, can we be in a position to make some of these difficult choices (without guilt!).

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

The Confrontation Awaits

One of my kids has a fear. To me, it's a silly fear, but to him, it's crippling. Over the past few days, he's spent much time trying to avoid facing this fear. Heck, if he had his way, he could simply avoid it altogether for the next 80 years and die a happy man.

One of my kids has a fear. To me, it's a silly fear, but to him, it's crippling. Over the past few days, he's spent much time trying to avoid facing this fear. Heck, if he had his way, he could simply avoid it altogether for the next 80 years and die a happy man.

Secretly, I'd love to find ways, organically or not, to create opportunities for him to face his fear head-on. The moment he conquers this fear will be the moment he unlocks something powerful inside him. It reminds me of a conversation he and I shared a while back:

"Dad, what are you most scared of?"

"Public speaking."

"That's weird, you speak all the time. Don't people pay you money to speak?"

"Yeah, they do!"

"Why do you do that if it's your biggest fear?"

"Why do you think I started? I did it BECAUSE it was my biggest fear."

I won't sit here on my high horse claiming to be the most courageous person in the world. I'm just a dude with a bunch of silly fears who has a track record of getting better and more impactful each time I face these fears head-on.

As I see it, our fears are often one of the few barriers between us and our dreams. Between us and our callings. Between us and our meaning. If that's true, why are we going to let a silly little fear be what stops us?!?!

On most days, I spend time with people who are trying to decide whether to let their fears hold them back from living their best life. Sometimes, the person on the other end of those conversations is the person I'm staring at in the mirror.

Fear is inevitable. It won't go away. We won't grow out of it. Instead, it shifts. It takes different forms. It manifests itself in new ways. But it's here to stay. If that's true, we might as well face it head-on!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

$50K On the Kitchen Table

"I don't care if you buy this vehicle," I told them. "However, if you decide to buy it, use cash. Please don't fall into this trap again."

More than three years ago, I wrote about something I call the "pile of cash test." It's a little behavioral hack that can help us combat the psychological warfare caused by debt. You can read the original piece at the link above.

Well, I've used the pile of cash three times in the past month. Most notably, I have one particular story to share with you. One of my clients wanted to purchase a new vehicle, around $65,000. After accounting for their trade-in, the remaining amount due was $50,000.

I think we can all agree that $50,000 is a lot of money. Therefore, they naturally decided to finance it. Whoa, whoa, whoa!!!! I was walking alongside them while they painfully and frustratingly paid off a ton of debt, and now they want to go back into $50,000 of debt to buy a vehicle?!?!

"I don't care if you buy this vehicle," I told them. "However, if you decide to buy it, use cash. Please don't fall into this trap again."

"I don't think we would feel comfortable taking $50,000 out of savings to do this," they responded.

"I guess you don't want the vehicle that badly, then." That comment didn't go over well.

They were still waffling when we left the room. That's when I gave them the pile of cash test challenge. Go to the bank, withdraw $50,000, set it on the kitchen table, then decide how important that vehicle is.

It wasn't easy for them to withdraw $50,000 from their bank, but they did it!!! They even joked that it felt like they needed to hire armed bodyguards just to have it in their home.

The result? Here's what they wrote back: "It was an eye-opening experience. To be honest I'm not sure we could ever spend $50,000 on a car ever again after doing that. It puts much in perspective. I think we need more contentment or more humility. Maybe both."

The pile of cash test never fails. Put this one in your toolbelt for a rainy day. It just might come in handy if you're ever in need of a fresh perspective.....or a fun behavioral science experience.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

OK, But Where You Gonna Get 9%?

The U.S. stock market has delivered a return of over 9% annually (and 10% annually over the last 100 years). Almost every time I discuss this topic, someone snidely asks, "OK, but where you gonna get 9%?"

My simplification of investing principles and practices is one of the most heavily criticized topics I write and podcast about. Here, I'll give you the quick elevator speech: Patiently invest in a cheap, broad, total U.S. stock market index fund. Invest early, contribute regularly, never sell, do nothing, remain patient, don't meddle, and let the market take care of the rest. See, simple! I've also written many times about how the 155-year history of the U.S. stock market has delivered a return of over 9% annually (and 10% annually over the last 100 years). Almost every time I discuss this topic, someone snidely asks, "OK, but where you gonna get 9%?"

That would be a fair question, except for the fact that we discuss it regularly! "A cheap, broad, total U.S. stock market index fund." Examples could include VTI, VTSAX, or FSKAX. This isn't a theory. It's not some hypothetical. It's not a case study that looks good on paper but is difficult to put into practice.

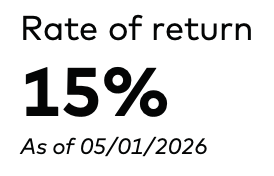

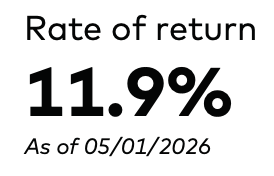

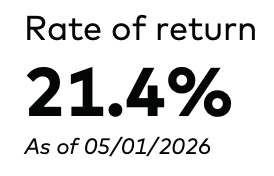

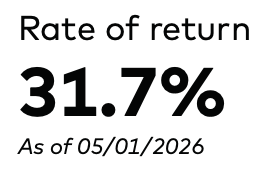

Today, I'll open the books of my life. For the past 15 years, my investment accounts have held one thing and one thing only: "A cheap, broad, total U.S. stock market index fund." I've made zero changes. I spend literally no time managing it. I give zero consideration to the ups and downs of the market. I never consider tweaking or meddling. What do I have to show for it? I'll show you.

My investment account updates the annualized return numbers at the end of each month. Given that April just concluded, I jumped into my account to see where they stand, and here's what I found:

Over the past 10 years: 15.0% per year

Over the past 5 years: 11.9% per year

Over the past 3 years: 21.4% per year

Over the past 1 year: 31.7% on the year

I'm not trying to beat the drum of "building wealth" or getting rich, but rather, I want people to understand 1) how real this is, and 2) how simple these principles really are. If we're going to invest, we might as well be good stewards of the resources we're blessed with.

Where you gonna get 9%? Right here. Right in front of us. While we don't know what the future will hold, the last 155 years tell us that, yes, it will be messy, but also yes, it will be rewarding. Stay patient. Stay simple.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Playing Us Like a Fiddle

I recently did a little informal survey on my Instagram account. Here was the question: "Without looking, how do you think the U.S. stock market has performed over the last 12 months?"

I love watching how the mainstream media and social media talk about the stock market. When the markets are going through a tough spell, people (hysterically) talk about it. The world is ending! The world is ending! You're all screwed!!! Yet, when the market is doing well, crickets.

I recently did a little informal survey on my Instagram account. Here was the question: "Without looking, how do you think the U.S. stock market has performed over the last 12 months?"

70% of respondents said the market was down. 20% said the market was up. 10% said it's about the same. On average, respondents said the market is down by approximately 9% over the past 12 months. How did they do?

At yesterday's market close, the U.S. stock market was up 32% over the past 12 months (up nearly 34% after accounting for dividends). Strange, isn't it? The overall sentiment is that the stock market is burning, while in reality, it's hitting new all-time highs. The stock market has nearly doubled over the past five years, yet we think the world has already collapsed.

They are playing us like a fiddle! From a behavioral science perspective, we see what we want to see. If we have a negative tint to our lens, we'll find the negative. If we have a positive tint to our lens, we'll find the positive. Today, our culture thrives on a negative lens, and the media all around us is more than happy to help us indulge.

One young man who answered my question guessed that the market is up 30%. He practically nailed it! I voiced my surprise that he knew this and shared why I was conducting this little study: "Oh, I don't watch the news or follow social media."

In other words, nobody played him like a fiddle. He was basing his answer on whatever information (you know, facts) he had available. He was able to cut out the noise, remove the biased lenses, and try to answer my question based on practical thought. Somehow, that's a crazy concept in modern-day America. It's a wild world when we can be more in tune with reality by absorbing less content.

One money-related takeaway. Open your investment account. See for yourself. If you're investing well (i.e., broad, low-cost stock market index funds), you should see your balances at an all-time high. Never before in your life have the balances been at this level. Celebrate that. Know it's true. Also know that rough times will, in fact, come. That's okay, though, as it's all part of the journey.

Lastly, and most importantly, try to muffle the noise, live a meaningful life, and don't let the day-to-day craziness of the media or the stock market mess with you. Life's too short to obsess over the things we can't control.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Excuses

Excuses are the gateway drug to more excuses. I know that if I skip today, it will provide my brain with the necessary cover to skip again....and again.....and again.

Fever, migraines, hallucinations. It's been a rough 12 hours in my little corner of the world. I was struck by a sickness that knocked me right off my feet. If you read my blog via e-mail, you were probably wondering why you didn't receive it at the normal time. Well, it was because I was having visions of unicorns riding in Jeeps while blasting Ace of Base on the stereo. Well, I'm not sure that was the exact hallucination, but you get the point.

It's an honor to write this blog each day, and I sincerely apologize for the late delivery. It's one of the greatest honors of my life, and I never take that for granted. It would be so easy for me to skip a day on my writing. It would be my first skip since I started this blog nearly 1,300 days ago. I have all the excuses in the world to skip. Except for one problem: I hate excuses.

Excuses are the gateway drug to more excuses. I know that if I skip today, it will provide my brain with the necessary cover to skip again....and again.....and again.

I don't say this from a position of intelligence and wisdom, but rather self-inflicted, self-sabotaging experience. I've experienced first-hand what it looks like to use excuses. The moment we humans decide to use an excuse, we're giving ourselves an out from our promise to ourselves, from our personal responsibility, from our mission.

It's why I write every single day, no excuses. It's why I take 10,000+ steps every single day, no excuses. It's why I step onto my biometric scale every day, no excuses. It's why I intermittent fast every single day, no excuses. It's why I refuse to take early morning meetings that would prevent me from spending quality time with my kids, no excuses. It's why Sarah and I complete a budget every single month, no excuses.

Excuses are the gateway drug to more excuses. Whatever you're up to this week, no matter how many excuses you have to mail it in, don't allow that to happen. Yes, life is hard. Yes, very real situations arise that can feel like the universe kicking us while we're down. All that is true. But we don't have to let the excuses win. The impact that you're going to make, the meaning that you'll live with, and the mission you're following are far bigger than whatever excuses come your way. Keep going!

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Obsess About the Inputs

As a society, we're obsessed with outputs. How much profit a company makes. How many clients we can attain. How much we'll make on the other side of that next promotion. The grade we get on our report card. If our team won. Regardless of the arena of life, we're obsessed with the outputs.

One of the primary principles I teach to families and businesses is counter-cultural. As a society, we're obsessed with outputs. How much profit a company makes. How many clients we can attain. How much we'll make on the other side of that next promotion. The grade we get on our report card. If our team won. Regardless of the arena of life, we're obsessed with the outputs.

I hate obsessing over outputs. Instead, I suggest we ought to obsess about the inputs and measure the outputs. The outputs are the outputs, which we often cannot control. However, we can absolutely control (or at least influence) the inputs. In fact, this is one of the primary drivers of Northern Vessel. When we first started the company, TJ mentioned that one of his desired outputs was to someday sell 400 cups in a day. As he explained, most coffee shops sell 100-200 cups per day. If we could ever find a way to get to 400 cups, that would be massive.

Rather than trying to sell 400 cups in a day (the output), we put 100% of our time, resources, and energy into the inputs:

Creating an excellent product.

Developing systems to ensure consistency.

Cultivating a team culture that would allow that to happen.

Building the means to scale volume efficiently.

Practicing world-class hospitality.

Curating a brand that people can recognize and relate to.

It took more than two years, but after obsessing about the inputs day in and day out, we finally hit 400 cups in a day! It was such a fun accomplishment. We measured it....and celebrated.

Then, something happened. We averaged 400 for a week. Then 400 for a month. Then, in a wild turn of events, we averaged 400 for a year. We even had a day we served 500 cups! In January, we sold 600 cups in a day! A week later, we sold 700 cups in a day! Then, just a few weeks ago, we sold 800 cups in a day! Our brains are melting....

We dreamed of someday serving 400 cups in a single day, and now live in a reality where 800 cups are on the table. We NEVER obsessed about selling 400 (never mind 800) cups. We obsessed over the inputs.

The same goes for all areas of life. My kids had lacrosse and football games this weekend. Frankly, I don't care whether they win or lose. I don't even care about what individual accomplishments they achieve during the games. I obsess about four inputs:

Play hard.

Practice good sportsmanship.

Listen and obey.

Have fun.

If they control those four inputs, they won (regardless of the scoreboard). Obsess about the inputs, measure the outputs.

This principle is about as counter-cultural as anything I talk about here, but I believe in it so much. Control what we can control, and let the cards fall as they may. Words to live by. Therefore, no matter the outcomes you experienced today or this week, focus your energies on the inputs that go into it, not the eventual outcome. If you do that long enough, you just might like the outcomes.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.

Getting Back Into His Cage

His mental health is eroding quickly. Dark thoughts are starting to seep in. His breaking point might be approaching.

Note: This is a sensitive story, but fortunately for countless readers, I've been granted permission to share it here.

A man asked to meet with me. Mid-40s. Married. Three children. Above-average household income. Average house. Pretty standard lifestyle: not too bougie, but also not perceived as frugal.

Here's the short version of the situation. He's beyond stressed. Finances are causing tremendous friction in his marriage. His wife wants to stay home with the kids, but they can't make it work. He's embarrassed. He feels like a failure. He's miserable. He hates his job. He wakes up each day dreading what's about to happen. He can't leave, though, as his current income exceeds other known options. His mental health is eroding quickly. Dark thoughts are starting to seep in. His breaking point might be approaching.

As our conversation progressed, I started asking him probing questions to identify the true stress points. For several minutes, nothing he said alarmed me.....all normal stuff. Then, we found it.

"Tell me about the vehicles. Do you have any vehicle debt?"

"My truck payment is around $1,300, and my wife's SUV is $800 per month."

There it is! $2,100 per month on vehicle payments alone. All of this pain, suffering, misery, and struggle, only to boil it down to a few key decisions. I challenged him on these decisions.

"Our vehicles aren't nearly as nice as some of our friends and family."

"I'm a truck guy. I can't help that I like nice trucks."

"I want my wife to be safe. We need something reliable."

I have a rhetorical question for you. Do you believe the three sentiments above merit wrecking one's entire life, marriage, financial structure, and mental health? The answer is a resounding NO!!! Of course it's not, but millions of Americans live in this reality daily.

Everything he and his wife have ever dreamed of lives on the other side of these vehicles. These vehicles are cages! They've been snared in the trap. They unknowingly locked themselves in a life they don't want to live. The cage might not have metal bars, but it might as well. I made my case for a different set of decisions, trying to illuminate what an alternate reality could look like: their dream life. However, it requires them to destroy the cages.

After the meeting, I walked outside with him, shook his hand, and watched him get back into his cage. I gotta admit, it was a pretty sweet truck. Clean, fresh wax, enormous in stature. But a cage, nonetheless.

We all have cages. It might not look like a truck, but it's something. My challenge to you today is to look at yourself in the mirror and identify your cage. Something that is (or could) hold you back from living the life you deserve to live. It's an uncomfortable exercise, and not always as obvious as it seems. I've had my share of cages over the years, and I suspect you do, too.

Smash the cage.

____

Did someone forward you this post? We're glad you're here! If you'd like to subscribe to The Daily Meaning to receive these posts directly in your inbox (for free!), just CLICK THIS LINK. It only takes 10 seconds.